Search “top fintech companies 2026” and you get the same article forty times. A ranked list of software development companies like Vention, ELEKS, SDK.finance, Netguru. Every one of them tells you who builds fintech software.

The issue is, they do not tell you who is actually using it.

That gap is the biggest challenge for anyone selling into financial technology. If you sell fraud tooling, a core banking module, a settlement rail, or a data layer, you do not care which agency builds the software. You care about which enterprise has Fiserv integrated into its issuer stack, which marketplace adopted Stripe two years ago and is now reaching its limits, and which mid-market bank is still relying on a legacy core system it is eager to replace.

That is technographic data and it is the difference between building a targeted pipeline and sending a spray of cold emails into the void.

This is not a vendor directory. It is a map of the fintech software install base.

Below are 100 companies organized by the fintech software categories they use, along with the specific integrations powering their operations and the use cases behind them. Find the category that aligns with your product, and you have found your ICP.

01Why “who builds it” lists are useless for sales

02The 4 Technical Buckets (how to read this list)

03Bucket 1: Embedded Finance & Payments Infrastructure

04Bucket 2: AI Orchestration & Ops Automation

05Bucket 3: Core Banking & Infrastructure Solutions

06Bucket 4: Real-Time Settlement & Treasury Management

07The Technographic Targeting Play (4 steps)

Why “Who Builds It” Lists Are Useless for Sales

Here is a number that should change how you think about every prospect list you own. Sales reps spend 27.3% of their time dealing with inaccurate data, according to ZoomInfo research cited across the industry. That is 546 hours per rep per year, more than 13 full working weeks, spent chasing wrong numbers and stale records.

|

27.3%

of rep time lost to inaccurate data

|

546

hours per rep per year, over 13 work weeks

|

22.5%

annual B2B data decay, about 2.1% a month

|

Now layer on the decay rate. B2B data degrades at roughly 22.5% per year, about 2.1% per month, and it compounds silently whether you touch the record or not (per Validity’s 2025 State of CRM Data Management report and multiple provider benchmarks). By December, one in four records you rely on is wrong. Wrong title, wrong email, or the company abandoned the tech stack you targeted them for eighteen months ago.

That last point is the killer for technographic selling. A prospecting list built on stale install-base data does not just waste outreach. It sends you after the wrong problem. You pitch a Stripe migration to a company that ripped out Stripe last year. You lead with a core-banking replacement to a bank that finished its Temenos cutover in Q1. The filter looked precise. The data underneath was rotting.

Generic “top fintech companies” content makes this worse, not better, because it gives you names with zero stack intelligence. A name is not an ICP. A name plus a verified integration plus a use case is an ICP. That is what the next four sections give you.

The value is not the company name. It is the technographic profile: the software they run, the integration that proves it, and the use case that tells you what they are trying to solve. That is the layer competitors cannot copy from a Google search.

See what a continuously verified, install-base dataset looks like before you spend another hour chasing stale records.

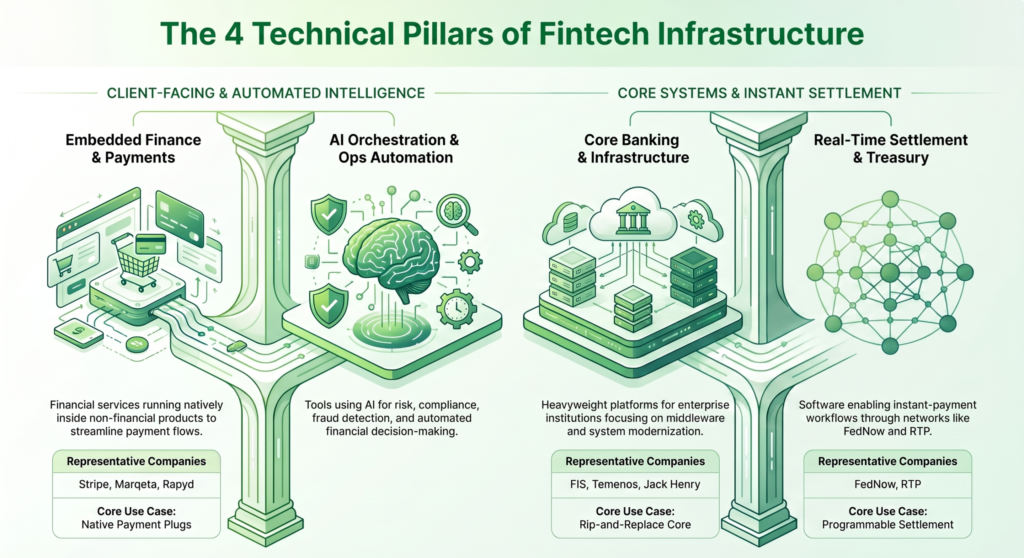

The 4 Technical Buckets and How to Read This List

We grouped 100 companies by what kind of fintech software they run, not by industry or size. Each bucket maps to a different buyer, a different pain, and a different pitch.

Embedded Finance & Payments Infrastructure

Companies running payments and financial services natively inside a non-financial product.

Sell anything that plugs into a payment flow? This is your bucket.

AI Orchestration & Ops Automation

Companies using AI for fraud detection, KYC/AML, underwriting, and automated financial decisioning.

Sell risk, compliance, or decisioning tooling? Start here.

Core Banking & Infrastructure Solutions

Mid-market to enterprise institutions running heavyweight core platforms.

Sell modernization, middleware, or a rip-and-replace core? These are your accounts.

Real-Time Settlement & Treasury Management

Companies live on FedNow, RTP, or programmable settlement and treasury workflows.

Sell instant-payment enablement, treasury software, or reconciliation? This bucket is heating up fast.

Each entry below follows the same technographic format: Company. Fintech integration. Use case. That structure is the point. It is what a real install-base list looks like.

A note on method: integrations below reflect publicly disclosed partnerships, press releases, and product announcements. Company-to-vendor relationships change. The full, multi-verified, continuously refreshed version of this mapping is a dataset, not a blog post, and that distinction matters more than anything else on this page.

Embedded Finance & Payments Infrastructure

The category that quietly eats everything. Embedded finance lets any platform offer banking, cards, or payments without becoming a bank. If your product touches a checkout, a payout, or a card program, every company here is a live target.

DoorDash partnered with Fiserv to embed formal banking services into the Dasher app through the Crimson program. The integration enabled instant post-delivery payouts, a full deposit account, and driver-focused financial services, with Starion Bank serving as the sponsor bank.

Use case: Embedded payouts and gig-worker banking portals.

This is the template: a non-financial platform, a payments infrastructure partner, and a financial product embedded directly inside the app.

| # | Company | Fintech Integration | Use Case |

|---|---|---|---|

| 1 | DoorDash | Fiserv (Crimson program, Starion Bank sponsor) | Embedded driver banking + instant payouts |

| 2 | Uber | Marqeta card issuing, Branch/partner rails | Driver debit, instant earnings access |

| 3 | Shopify | Stripe (Shopify Payments), Shopify Balance | Embedded merchant payments + banking |

| 4 | Lyft | Payfare/partner banking, Mastercard debit | Driver instant pay + financial portal |

| 5 | Instacart | Stripe payments infrastructure | Marketplace checkout + shopper payouts |

| 6 | Amazon | Custom + Stripe/partner rails | Marketplace payments, seller disbursement |

| 7 | Toast | Embedded payments + Toast Capital | Restaurant POS payments + merchant lending |

| 8 | Klarna | Proprietary BNPL + card issuing | Point-of-sale installment financing |

| 9 | Affirm | Proprietary BNPL rails, card program | Embedded checkout financing |

| 10 | Mindbody | Embedded payments platform | Wellness studio billing + payments |

| 11 | ClassPass | Stripe subscription + payments | Recurring membership billing |

| 12 | Squarespace | Stripe / Square integrations | Creator commerce + checkout |

| 13 | Wix | Wix Payments (Stripe/adyen backend) | SMB storefront payments |

| 14 | Substack | Stripe Connect | Creator subscription payouts |

| 15 | Patreon | Stripe Connect payouts | Creator recurring revenue |

| 16 | Deliveroo | Adyen payments | Marketplace order settlement |

| 17 | Grab | Proprietary GrabPay + partner rails | Super-app embedded wallet |

| 18 | Gojek | Embedded GoPay wallet | Super-app payments + financial services |

| 19 | Airbnb | Adyen / Stripe payout rails | Host disbursement + guest checkout |

| 20 | Etsy | Adyen (Etsy Payments) | Marketplace seller settlement |

| 21 | Wayfair | Enterprise payments + BNPL partners | Checkout financing |

| 22 | Chewy | Payments + Autoship billing | Subscription commerce |

| 23 | Zocdoc | Stripe healthcare payments | Patient billing embed |

| 24 | Faire | Embedded net-terms financing | B2B marketplace credit |

| 25 | Flexport | Embedded trade finance | Freight financing + payments |

So what? Every company in this bucket already crossed the “we do payments now” threshold. That means their next problem is optimization: fraud on the new volume, reconciliation across rails, or a second financial product. If you sell into the layer above the payment rail, these are companies with budget already unlocked and a live pain waiting.

AI Orchestration & Ops Automation

Fraud detection, KYC/AML, underwriting, and automated decisioning are where AI has moved beyond experimentation and become a core operational function. This is where AI stopped being a slide in a strategy deck and became a budget line item.

The buyers here are Heads of Risk, Chief Compliance Officers, and VPs of Fraud, teams overwhelmed by false positives, manual review queues, and the growing complexity of financial crime operations.

Position AI as an operational partner, not just another software tool. Its effectiveness depends entirely on the quality and relevance of the data powering it. An AI fraud engine running on outdated identity data is like a sports car running on contaminated fuel: powerful technology, but limited by what feeds it.

That framing creates the entry point into every account listed below.

| # | Company | Fintech Integration | Use Case |

|---|---|---|---|

| 26 | Stripe | Radar (proprietary ML fraud) | Real-time transaction fraud scoring |

| 27 | PayPal | Proprietary AI risk + Simility | Fraud detection, dispute automation |

| 28 | Block (Square/Cash App) | In-house ML risk models | Fraud + AML monitoring |

| 29 | Plaid | Signal + Identity Verification | Account risk, KYC orchestration |

| 30 | Coinbase | In-house + chain-analytics partners | Transaction monitoring, AML |

| 31 | Robinhood | ML surveillance + KYC vendors | Trade surveillance, onboarding |

| 32 | Chime | Fraud ML + partner KYC | Account-opening fraud prevention |

| 33 | SoFi | AI underwriting models | Automated lending decisions |

| 34 | Upstart | Proprietary AI underwriting | ML-based loan approval |

| 35 | Nubank | In-house AI credit models | Credit decisioning at scale |

| 36 | Revolut | AI fraud + transaction monitoring | Real-time fraud interdiction |

| 37 | Wise | ML risk + compliance automation | Cross-border AML screening |

| 38 | Marqeta | Risk controls + tokenization | Card fraud, spend controls |

| 39 | Ramp | AI spend + receipt automation | Automated expense + fraud flags |

| 40 | Brex | ML underwriting + spend controls | Corporate card risk decisioning |

| 41 | Mercury | Risk engine + KYB automation | Business onboarding compliance |

| 42 | Klarna | AI risk + BNPL underwriting | Real-time credit decisioning |

| 43 | Affirm | ML underwriting models | Point-of-sale credit scoring |

| 44 | Kabbage/Amex | AI SMB underwriting | Automated small-business lending |

| 45 | Deserve | AI credit + card decisioning | ML card issuance |

| 46 | Alloy | Identity decisioning platform | KYC/KYB orchestration layer |

| 47 | Socure | AI identity verification | Fraud + identity scoring |

| 48 | Persona | Identity verification workflows | Onboarding KYC automation |

| 49 | Feedzai | AI financial crime platform | Enterprise fraud + AML |

| 50 | Sardine | Fraud + compliance ML | Real-time behavioral risk |

| 51 | Hummingbird | AML case management | Compliance investigation automation |

| 52 | Unit21 | Risk + AML orchestration | Automated case + rules engine |

| 53 | ComplyAdvantage | AI AML screening | Sanctions + transaction monitoring |

| 54 | Taktile | Decision automation platform | Credit + risk decision workflows |

So what? These companies do not need to be convinced that AI matters. They need the underlying input layer to be accurate, reliable, and clean. The pitch that resonates is not “add AI.” It is: “Your AI is only as accurate as the identity and firmographic data powering it.” That reframes a crowded AI market into a data infrastructure problem, and that is where the real leverage lies.

Core Banking & Infrastructure Solutions

The unglamorous foundation. Mid-market and enterprise institutions running heavyweight core platforms. Long sales cycles, deep switching costs, and enormous contract value. The buyer is a CIO, a Head of Payments, or a core-transformation program lead who has been fighting a legacy system for years.

Enterprises are consolidating fintech vendors aggressively. The average enterprise runs six to ten payment vendors, each with its own integration and maintenance burden (per Modern Treasury’s 2026 predictions). Integration debt is the pain. If your product reduces vendor sprawl or modernizes the core, every institution here is carrying that weight right now.

| # | Company | Fintech Integration | Use Case |

|---|---|---|---|

| 55 | Wells Fargo | FIS + internal core | Core deposit + payment processing |

| 56 | Citizens Bank | RTP + treasury core | Commercial banking infrastructure |

| 57 | Truist | Core modernization program | Post-merger core consolidation |

| 58 | Fifth Third | Fiserv + modernization | Retail + commercial core |

| 59 | Regions Bank | FIS core platform | Deposit + lending core |

| 60 | KeyBank | Enterprise core + payments | Commercial banking stack |

| 61 | Huntington | Core + digital banking layer | Retail banking infrastructure |

| 62 | M&T Bank | Core banking modernization | Deposit processing |

| 63 | Varo Bank | Temenos-class core (neobank charter) | Full-stack digital bank core |

| 64 | Green Dot | BaaS core infrastructure | Banking-as-a-service platform |

| 65 | Bancorp | BaaS + sponsor-bank core | Embedded finance sponsor rails |

| 66 | Cross River | Core + API banking platform | Fintech sponsor-bank infrastructure |

| 67 | Column | Developer-first core banking | API-native bank infrastructure |

| 68 | Coastal Community Bank | BaaS core (fintech sponsor) | Sponsor-bank programs |

| 69 | Pathward | BaaS + core platform | Embedded banking sponsor |

| 70 | Axos Bank | Digital-first core | Online banking infrastructure |

| 71 | Live Oak Bank | Finxact/Jack Henry-class core | SBA lending + digital core |

| 72 | Customers Bank | Core + real-time platform | Commercial + fintech banking |

| 73 | Grasshopper Bank | Modern API core | Digital SMB banking |

| 74 | Mercury (BaaS partners) | Sponsor-bank core stack | Business banking infrastructure |

| 75 | Dave | Core + partner-bank rails | Neobank infrastructure |

| 76 | MoneyLion | Core + embedded finance stack | Consumer financial platform |

| 77 | Current | Partner-bank core | Digital banking infrastructure |

| 78 | Bluevine | Core + SMB lending platform | Business banking + credit |

| 79 | Novo | Partner-bank core | SMB digital banking |

| 80 | Relay | Core banking + multi-account | SMB financial operations |

So what? Core transformation is a multi-year, multi-million-dollar commitment. The reps who win in this space do not sell features; they enter conversations already knowing which core system the institution runs, when the contract is up for renewal, and what integration debt is slowing down the roadmap. That level of intelligence is technographic data, and it is exactly what a raw name list cannot provide.

Real-Time Settlement & Treasury Management

The fastest-moving bucket in 2026. Companies live on FedNow, RTP, or programmable settlement and modern treasury. Adoption just crossed from experiment to standard.

|

1,500

FIs on FedNow, late 2025

|

58%

of instant-pay banks run both RTP and FedNow

|

40%+

of $100M+ firms already use RTP

|

~70%

expect to adopt within two years

|

Roughly 1,500 financial institutions are on FedNow as of late 2025, and 58% of U.S. banks that enable instant payments now run both RTP and FedNow (per Softjourn and Federal Reserve data). More than 40% of companies over $100M in revenue already use RTP, and nearly 70% of businesses expect to adopt instant payments within two years (U.S. Bank study via Dwolla).

Translation: the buyers here are moving now, and the ones who have not moved are feeling the pressure. This is the bucket where “why now” writes itself.

| # | Company | Fintech Integration | Use Case |

|---|---|---|---|

| 81 | JPMorganChase | RTP (founding), FedNow, in-house treasury | Real-time corporate settlement |

| 82 | Citizens Bank | RTP (since 2019), treasury platform | Commercial instant payments |

| 83 | US Bank | RTP + FedNow enablement | Corporate instant disbursement |

| 84 | PNC | RTP + treasury management | Commercial real-time payments |

| 85 | BNY | Network-level fraud + real-time rails | Institutional settlement |

| 86 | Wealthfront | RTP + FedNow withdrawals | Instant account transfers |

| 87 | Dwolla | Single API to RTP + FedNow | Embedded pay-by-bank for enterprises |

| 88 | Modern Treasury | Payment ops + programmable settlement | Treasury + money-movement automation |

| 89 | Finzly | ISO 20022-native, all-rails platform | Unified FedNow/RTP/ACH/Fedwire |

| 90 | Volante Technologies | Payments hub + ISO 20022 | Real-time payment processing |

| 91 | Metropolitan Commercial Bank | ACH cloud migration (Finzly) | Payments modernization |

| 92 | Jack Henry | FedNow + RTP enablement | Community-bank instant payments |

| 93 | ACI Worldwide | Real-time payments platform | Enterprise + bank settlement |

| 94 | Temenos | Payments hub + core | Bank real-time processing |

| 95 | Trovata | AI treasury + cash management | Automated cash forecasting |

| 96 | HighRadius | AI treasury + O2C automation | Receivables + reconciliation |

| 97 | Tesorio | Cash-flow + treasury platform | Working-capital automation |

| 98 | Circle | USDC programmable settlement | Stablecoin treasury + cross-border |

| 99 | Fireblocks | On-chain settlement infrastructure | Digital-asset treasury + custody |

| 100 | Stripe (Treasury) | Programmable treasury + settlement | Embedded treasury for platforms |

So what? Instant-payment adoption is the clearest “why now” trigger in fintech right now. A company that just went live on FedNow has a fresh reconciliation problem, a new fraud surface, and a treasury workflow that needs rebuilding. Timing outreach to that live event is worth more than any amount of persona guessing. But you can only time it if your data flags the change the moment it happens.

These 100 companies are a preview. The full dataset covers thousands, mapped to verified decision-makers and refreshed continuously.

Filter by software category, revenue band, geography, and buying signal to reach your exact ICP at the right moment.

Get the Full DatasetTalk to Our Data Team →

The Technographic Targeting Play (4 Steps)

A list is static. A play is repeatable. The goal is not just to identify companies, it is to turn install-base intelligence into a predictable pipeline. Here is the four-step framework to put that intelligence into action.

Step 1: Match your product to the right bucket

Do not target “fintech companies” as a broad category. Target the specific fintech segment where your product solves a clear operational challenge.

Precision beats volume every time. The closer the match between your product and the technology gap, the stronger the buying signal.

Step 2: Filter by the integration, not the industry

The strongest signal is not “companies in fintech.” It is companies running a specific technology that have a gap your product can solve.

For example, if you sell sales engagement software, a company running Salesforce without a sequencing platform represents a clear opportunity. The same logic applies across fintech categories. The technology stack reveals the opportunity. The integration points reveal where the gap exists.

Step 3: Time outreach around stack events

Technology changes create buying windows. A new FedNow Service rollout, an embedded payments launch, or a core transformation announcement creates a “why now” moment.

These signals are time-sensitive and often lose relevance within weeks. Reaching a company shortly after it announces a major technology shift is significantly more effective than approaching it a year later. This only works when your data is continuously updated rather than sitting as a static list.

Step 4: Enrich before you engage

With B2B data decaying at roughly 22.5% annually, any record that has not been verified recently carries increasing risk. Re-verify data at the point of outreach rather than relying on periodic cleanup.

The teams that treat data as a continuously maintained system, rather than a one-time purchase, build stronger pipelines and make better targeting decisions. Everyone else is running outbound on assumptions.

Match the bucket. Filter by the install. Time the trigger. Enrich continuously.

That is technographic selling. It is not more work than spray-and-pray outreach, it is more efficient, because it eliminates wasted effort caused by poor-fit accounts and outdated data. In fact, sales reps spend an estimated 27% of their time dealing with poor-quality data and related inefficiencies, time that can be redirected toward higher-intent opportunities when the right intelligence is in place.

Where This List Ends and Your Dataset Begins

One hundred companies are a starting map. They provide direction, but they are not the full territory.

The moment you begin executing the play above, the limitations of a blog post become clear. A static table cannot:

That is the difference between content and infrastructure. This article provides the market view about the companies, categories, and fintech stacks shaping the landscape. To fully access and act on this intelligence, you need a maintained dataset that includes:

The play requires infrastructure: a continuously refreshed, multi-verified install-base dataset mapped to real decision-makers and built to identify your exact ICP.

That is what Span Global Services builds

Not a list. An intelligence layer.

Frequently Asked Questions

Which companies use fintech software in 2026?

Thousands, and the useful way to map them is by category, not name. The four buckets: embedded finance and payments (DoorDash on Fiserv, Shopify on Stripe), AI orchestration (Stripe Radar, Feedzai, Alloy), core banking (Wells Fargo, Cross River, Column), and real-time settlement (JPMorganChase on RTP, Circle). The category tells you what problem each company is solving, which is what matters for targeting.

What is technographic data and why does it matter for fintech sales?

It maps the technology stack a company runs: which core platform, which payment rail, which fraud engine. It is one of the highest-signal inputs for ICP qualification because it reveals gaps and replacement windows. It turns “companies in fintech” into “companies running X that lack Y,” a far more precise target than any firmographic filter.

How accurate is this list of companies and their fintech stacks?

The integrations reflect publicly disclosed partnerships and announcements at the time of writing. Vendor relationships change and B2B data decays at roughly 22.5% per year, so any static list drifts over time. That is exactly why a continuously verified, multi-source dataset beats a static web page you cannot act on today.

How often does B2B install-base data need to be updated?

Continuously. Account data decays at about 2.1% per month, and reps already lose roughly 27% of their time to inaccurate data. Any record untouched for 90 days is a candidate for re-verification. Top teams treat data as a live feed with enrichment at the point of entry, not a one-time purchase that rots in the CRM.

Can I get contact data for the decision-makers at these companies?

Yes. This blog gives you company names and stack insights. The full dataset connects them to verified decision-makers, Heads of Risk, CIOs, VPs of Payments, with direct contact details, filterable by software category, revenue, geography, and buying signals. That is the layer the article does not provide and the dataset is built to deliver.

What is the difference between a fintech vendor list and an install-base list?

A vendor list ranks the companies that build fintech software. An install-base list maps the companies that run it. Hiring a developer? You want a vendor list. Selling into fintech to find your ICP? You want an install-base list. Almost every “top fintech companies” article is the former. This one is the latter.

Related Posts