Most “top B2B tech” lists rank by brand recognition. Useless when your buyer is a 13-stakeholder committee. This guide replaces the ranking with a five-tier Buyer-Signal Stack that maps each vendor to the committee seat that actually owns the decision: infrastructure, systems of record, experience, AI-native applications, and the intelligence substrate underneath all of it.

Best for: CMOs, CROs, demand gen leaders, and BD teams selling into the enterprise tech stack.

Why Every “Top B2B Technology Companies” List Hasn’t Been Reliable

Every list ranking the top B2B technology companies driving digital transformation names the same vendors: Microsoft, AWS, Salesforce, SAP, IBM, and ServiceNow. A CIO already knows that.

These lists aren’t made for marketers, sales teams, or service providers who have to get approval from a 13-stakeholder buying committee. They are made to rank well on search engines.

Here’s the reality in 2026: most high-revenue deals are happening online, buyers are using AI for research, and every deal involves a large committee with veto power. On top of that, fewer than half of digital transformation initiatives actually hit their targets.

So the real question isn’t “who’s on the list?” It’s which companies are equipped with the right buying capabilities, understand requirements, and are investment-ready, and which are still selling like it’s 2018.

This guide shows you the difference.

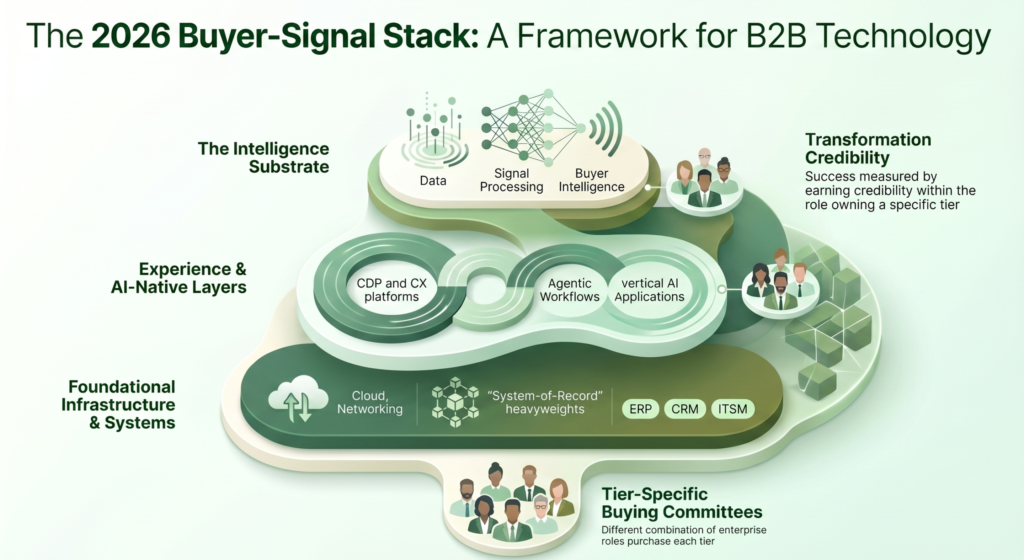

The Buyer-Signal Stack: A Framework for Evaluating B2B Technology Companies in 2026

The Buyer-Signal Stack is the five-tier framework we use at Span Global Services to map B2B technology demand. Each tier corresponds to a layer of the modern enterprise technology estate, and each tier is bought by a different combination of buying committee roles.

The five tiers:

A vendor is “driving digital transformation” in 2026 only to the degree that it earns credibility inside the buying committee role that owns its tier.

Across the 90M+ verified B2B contacts in our intelligence layer, the average enterprise technology evaluation now generates research footprints across 6 to 9 distinct job functions before a single sales rep is contacted. The “first-touch buyer” is dead.

Tier 1: Infrastructure Backbones

Microsoft Azure

Azure is the default infrastructure conversation in 2026, not because of technical superiority but because of bundle gravity. Most large enterprises already run on Microsoft 365, Active Directory, and GitHub. Azure rides those rails. Forrester reports 51% of information workers say their firms are now adopting Microsoft 365 Copilot, giving Azure an embedded AI workload path that competitors have to win through pure technical persuasion.

Amazon Web Services

AWS still owns the technical depth conversation. For workloads needing the broadest service catalog or specialized AI hardware access, AWS remains the safe choice. The 2026 challenge is FinOps credibility. CFO scrutiny on cloud spend has tightened, and Reserved Instance complexity now requires a specialist function inside most enterprises. Marketing to AWS-adopting accounts increasingly starts with verified AWS users data rather than broad cloud-buyer lists.

Google Cloud

Google Cloud has reframed itself around the AI infrastructure conversation. Gemini Enterprise integration into Google Workspace creates a parallel bundle motion to Microsoft’s. For technology buyers building agentic workflows from scratch, Vertex AI is increasingly the technical front-runner. The resistance is incumbency: most enterprises do not run their systems of record on Google Cloud.

Tier 2: System-of-Record Heavyweights

Salesforce

Salesforce remains the gravitational center of enterprise CRM in 2026, and the Agentforce launch has repositioned the platform from a system of record into an agentic execution layer. The Data Cloud + Agentforce + Industry Cloud combination is the most aggressive land grab in the CRM market this decade. The committee tension is total cost of ownership: CFOs increasingly question whether the Salesforce platform tax is justified when AI-native competitors offer 60% of the functionality at 30% of the cost. Reaching the Salesforce installed base for displacement plays remains one of the highest-intent demand motions in B2B.

SAP

SAP is the system-of-record default for global manufacturers and supply-chain-heavy enterprises. The 2026 story is Joule, SAP’s AI copilot, which expanded with fifteen specialized AI agents automating finance, supply chain, and HR workflows. For enterprises still on ECC, the forced 2027 migration deadline is creating one of the largest single transformation budgets in B2B technology. Vendors selling complementary ERP modernization tools or migration services to the SAP customer base have a narrow but lucrative window through 2027.

ServiceNow

ServiceNow has quietly become the most strategic IT platform purchase in the enterprise. What started as IT service management has expanded into HR service delivery, customer service workflows, and now the Now Assist AI layer that orchestrates work across departments. The committee that buys ServiceNow has grown from IT to a cross-functional decision including HR, customer service, and procurement.

Tier 3: Experience and Commerce Layer

Adobe

Adobe has positioned itself as the experience layer of the modern enterprise. The Adobe Experience Platform plus Real-Time CDP plus Journey Optimizer combination is a credible alternative to the Salesforce Marketing Cloud stack. Adobe was named a Leader in B2B customer data platforms in 2025, and the Deloitte Digital partnership announced in early 2026 specifically targets the B2B hi-tech buying group orchestration problem.

HubSpot

HubSpot’s relevance in 2026 is mid-market enterprise. For companies between USD 50M and USD 500M in revenue, HubSpot’s combined CRM, marketing automation, content, and commerce platform is increasingly outcompeting the “best of breed” stacks that mid-market companies used to build. The Breeze AI layer has made the platform agentic without forcing customers into a separate AI vendor decision.

Commercetools and Shopify Plus

The composable commerce conversation has matured. Commercetools owns the enterprise B2B composable commerce conversation, particularly in manufacturing and distribution where ERP integration depth matters more than front-end flexibility. Shopify Plus has expanded credibly into B2B and is now a serious option for mid-market manufacturers running hybrid B2B and DTC motions.

Tier 4: AI-Native Application Layer

This is the tier where 2026 is being redefined. The vendors below are not legacy companies adding AI features. They are companies architected from day one around agentic workflows.

OpenAI Enterprise and Anthropic

The foundation model conversation has split into two enterprise tracks. OpenAI’s enterprise product line, integrated into Microsoft 365 Copilot and standalone ChatGPT Enterprise, dominates general-purpose enterprise AI deployment. Anthropic’s Claude family has won the enterprise trust conversation around safety, governance, and long-context reasoning, particularly in financial services, legal tech, and code-heavy workflows.

Snowflake and Databricks

Both have completed the transition from data platform to AI platform. Snowflake’s Cortex AI and Databricks’ Mosaic AI are the two dominant ways large enterprises operationalize AI inside their existing data estate. The committee choice typically tracks to whether the organization is data-engineering-dominant (Databricks) or analyst-dominant (Snowflake).

Rippling

Rippling is the rare AI-native challenger that has displaced incumbents at scale. The employee graph technology that connects payroll, device management, app provisioning, and HR data into a single system has rewritten what mid-market HR tech buyers expect.

Tier 5: The Intelligence Substrate

Every tier above runs on data. Every AI agent above is only as effective as the data foundation underneath it. This is the tier that “top digital transformation companies” lists almost universally ignore, which is exactly why most digital transformation programs underperform their business targets.

The companies that win digital transformation in 2026 are not the ones with the biggest cloud bill or the most expensive AI stack. They are the ones whose data foundation can actually feed the AI agents accurate, timely, and verified buyer intelligence. Without that substrate, agentic AI in B2B selling becomes expensive guesswork dressed up as automation.

Forrester’s research on B2B AI deployment found that 73% of B2B buyers actively avoid irrelevant sellers. Relevance, in the agentic AI era, is no longer about better copywriting. It is about whether the data feeding the AI is verified, current, and contextually accurate. An AI SDR firing personalized sequences based on stale or fabricated contact data does not produce pipeline. It produces unsubscribes and brand damage. This is where disciplined B2B data cleansing shifts from back-office hygiene to a revenue-critical AI input.

Across 14 enterprise client engagements in 2025, the average lift in AI-driven outbound conversion from switching to a verified-contact intelligence foundation was 3.2x.

Not because the AI got smarter. Because the AI stopped working with bad inputs.

Conclusion

Digital transformation in 2026 is a stack decision, made by a 13-stakeholder committee, evaluated through multiple research channels, and underwritten by the quality of the intelligence layer feeding the entire system. The vendors above are the ones structurally aligned with this reality.

The strategic insight we operate by at Span Global Services: the AI agents, the cloud platforms, and the application-layer software all win or lose on the integrity of the buyer intelligence layer underneath them. That is the layer most lists ignore. That is also the layer that determines whether the rest of the stack delivers.

If you are mapping your next twelve months of B2B marketing or sales motion across this stack, and you want a view of where your target accounts actually sit across the buying committee evaluation, that is the conversation we have every day.

Frequently Asked Questions

Who are the top B2B technology companies driving digital transformation in 2026?

Why are most “top digital transformation vendors” lists unhelpful for buyers?

What role does data quality play in digital transformation success?

How long does an enterprise B2B technology purchase take in 2026?

What is the difference between digital transformation and B2B SaaS adoption?

How is AI changing the B2B technology buying process?

Which vendors are best for mid-market versus large enterprises?

Related Posts