Short answer: There is no single leader in smart clothing in 2026. The market has split into five competitive arenas, each with different winners, different buyers, and completely different go-to-market strategies. Treating smart clothing as one ICP is the fastest way to burn your 2026 budget.

Smart clothing is a specialized category within wearable technology – garments embedded with sensors, conductive fibers, and connected systems that collect data, deliver feedback, or adapt to user conditions. In 2026, this includes everything from wearable fashion and fitness apparel to clinical-grade biometric garments and industrial safety gear.

The current numbers justify the hype around this market segment. The global e-textiles and smart clothing market is valued at $22.08 billion in 2025, forecast to reach $29.23 billion in 2026, and projected to hit $274.99 billion by 2034 at a 32.34% CAGR, according to Precedence Research. Grand View Research pegs the narrower “smart clothing” segment at $7.40 billion in 2026, growing at 26.8% CAGR through 2033.

The growth is real. But the structure of the market is what matters.

A Chief Marketing Officer at a sports apparel brand, a procurement officer at a defense contractor, and a Chief Medical Officer at a hospital system are all technically buying “smart clothing.” They share almost nothing else in common. They do not evaluate vendors the same way. And they do not respond to the same messaging.

This guide breaks down the five arenas shaping the smart clothing market in 2026, who is actually leading in each arena, and what that means for anyone trying to sell into this market.

Table of Contents

- What Counts as Smart Clothing in 2026

- Arena 1: Consumer Fitness and Sportswear

- Arena 2: Clinical and Healthcare-Grade Biometrics

- Arena 3: Military, Defense, and Industrial Safety

- Arena 4: Luxury and Fashion-Tech Crossovers

- Arena 5: The Materials and Platform Layer

- The Five-Arena Framework: Why This Matters for B2B Go-to-Market

- FAQs

What Counts as Smart Clothing in 2026

Smart clothing technology includes apparel with integrated electronics, conductive fibers, or sensors that collect data, deliver feedback, or adapt to environmental or physiological conditions. The industry sorts products into three tiers:

- Passive smart clothing: Textiles that sense the environment (UV-reactive, temperature-regulating). This segment held 43% revenue share in 2025, per Grand View Research.

- Active smart clothing: Textiles that sense and respond, typically via embedded sensors with companion apps.

- Ultra-smart clothing: self-adapting systems that sense, process, and act, often with onboard machine learning or energy harvesting.

The definitional shift worth noticing: in 2026, the line between “clothing with a wearable attached” and “clothing as the wearable” has collapsed. Cornell University’s SeamFit research demonstrated 93.4% exercise-classification accuracy using conductive threads sewn into standard T-shirt seams, with collective fiber networks achieving 95% accuracy. Machine learning inference is now happening inside the garment itself.

This shift is what is pulling multiple industries into the same category at the same time. But the market does not behave as one unified space. It splits into 5 distinct arenas based on who is buying and why.

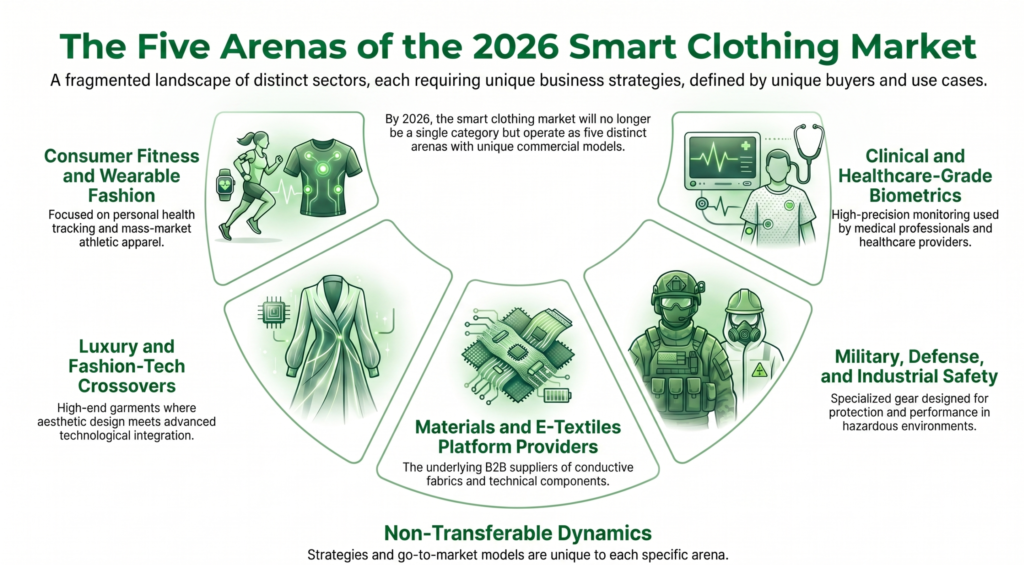

The Five Arenas of the Smart Clothing Market in 2026

The smart clothing market in 2026 does not operate as a single category. It functions as five distinct arenas, each defined by different buyers, use cases, and commercial models.

These arenas are:

· Consumer fitness and wearable fashion

· Clinical and healthcare-grade biometrics

· Military, defense, and industrial safety

· Luxury and fashion-tech crossovers

· Materials and e-textiles platform providers

Each arena has its own set of leading smart clothing companies, decision-makers, and go-to-market dynamics. What works in one does not translate to another.

Understanding this structure is critical. Without it, targeting “smart clothing companies” as a single audience leads to poor segmentation, weak messaging, and low conversion.

The sections below break down each arena, starting with consumer fitness and wearable fashion.

Arena 1: Consumer Fitness and Sportswear

Leaders: Nike, Under Armour, Adidas, Ralph Lauren, Wearable X (Nadi X), Sensoria, Athos.

This is the arena most people picture when they hear smart clothing. It is also the most crowded and the most mature.

The incumbents – Nike, Under Armour, Adidas compete on distribution, brand, and AI-driven performance features layered onto existing product lines. Under Armour’s Athlete Recovery Sleepwear and its broader connected apparel initiatives use partnerships with tech infrastructure players to scale features rather than invent the hardware.

The specialists have carved out category-defining products:

- Wearable X ships the Nadi X smart yoga pants with knitted accelerometers and haptic feedback at the hips, knees, and ankles. The pants correct yoga posture through gentle vibration, tested across 50 instructors of varying body shapes.

- Sensoria built its reputation on smart socks with textile pressure sensors, tracking cadence, foot landing technique, and running form. Its newer smart tights add hip-glute EMG for runners, and premium AI coaching runs about $4.99/month.

- Athos sells muscle-activity-tracking shirts and shorts used by professional sports performance institutes and is expanding into high school athletics. A full Athos kit runs close to $700.

The buyer: Consumer brand CMOs, fitness retail category managers, and DTC ecommerce leads. They care about the cost of customer acquisition, return rates, and whether the tech survives 100+ wash cycles (DuPont’s Intexar stretchable electronic ink is validated against that threshold).

Arena 2: Clinical and Healthcare-Grade Biometrics

Leaders: Hexoskin (Carre Technologies), Siren, Epicore Biosystems, Owlet, Xenoma.

This is where smart clothing stops being a lifestyle category and becomes a regulated medical device play.

Hexoskin is the clearest category leader. Its Astroskin platform is used in clinical cardiac, respiratory, and sleep research, and the company has validated its biometric shirt against medical-grade pneumotachograph and Polar H7 heart rate monitors in peer-reviewed studies. It works with NASA, the Canadian Space Agency, and SpaceX for space medicine applications, and maintains a cardiorespiratory data repository curated over a decade. This isn’t a moat a DTC brand can cross on marketing spend.

Epicore Biosystems entered a partnership with DuPont in May 2025 to accelerate technology-enabled apparel for worker health monitoring, signaling that the clinical arena is increasingly overlapping with industrial safety (more on that next).

The healthcare sector holds roughly 35% market share of smart textile applications, per 2026 industry reports, making it the single largest revenue concentration in the category.

The buyer: Chief Medical Officers at hospital systems, heads of clinical research at pharma companies, digital health VPs at payers, and procurement teams at medical device manufacturers. Sales cycles run 9-18 months. Regulatory and validation credentials do 80% of the selling.

Arena 3: Military, Defense, and Industrial Safety

Leaders: DuPont, Toray Industries, AiQ Smart Clothing, Schoeller Textiles, Gentherm, ThermoSoft.

Defense and heavy industry are the unsexy but highest-margin corners of smart clothing. North America dominated the smart clothing industry with over 38% revenue share in 2025, largely driven by defense procurement.

The U.S. military has announced field trials of AI-enabled textile systems in Arctic conditions covering more than 1,000 kilometers of testing. These aren’t pilots. They are operational readiness programs.

DuPont supplies the conductive inks, films, and component platforms that many consumer brands build on. Its Intexar stretchable electronic ink survives over 100 wash cycles in validated testing. The May 2025 DuPont–Epicore Biosystems partnership explicitly targets worker safety applications.

Toray Industries announced a September 2025 partnership with MAS Holdings to establish apparel manufacturing operations in India, with a new facility in Odisha expected to begin commercial operations in early 2026. The strategic layer: supply chain localization and sustainable manufacturing capacity to serve both consumer and defense contracts.

Gentherm operates as a thermal management specialist with dense patent coverage, and ThermoSoft has captured roughly 14.5% of the North American electric radiant heating market through its FiberThermics conductive fiber technology.

The buyer: Defense procurement officers, occupational health directors at oil and gas majors, and Chief Purchasing Officers at Tier 1 manufacturers. Deals are large, slow, and relationship-led. Compliance, durability, and validated test data are the entire conversation.

Arena 4: Luxury and Fashion-Tech Crossovers

Leaders: Google (Project Jacquard / Levi’s), Ralph Lauren, CuteCircuit, Ministry of Supply, Tommy Hilfiger.

This arena is the most visible and the least profitable per unit. It exists because fashion houses need signals of innovation, and tech platforms need fashion distribution.

Google’s Project Jacquard pioneered touch-sensitive woven fabrics and has appeared most famously in Levi’s Trucker Jacket, turning a sleeve into a phone controller. The product category has softened commercially, but established the technical vocabulary that every fashion-tech brand now uses.

Ralph Lauren is consistently named in market research among the top North American smart clothing players, leveraging its brand equity to price-position tech-integrated apparel at a premium.

Ministry of Supply ships the Mercury sweater with active thermal regulation and has built a reputation for business-casual smart apparel that works in an office setting. This is the quiet corner of the category where the unit economics actually work, because the buyer treats a $250 sweater as a premium wardrobe purchase, not a gadget.

The buyer: Fashion house innovation leads, luxury retailer category buyers, and brand DTC founders chasing tech-fashion press coverage. Campaigns here are PR-led more than performance-led, making CEO-level outreach more effective than mid-funnel marketing.

Arena 5: The Materials and Platform Layer

Leaders: DuPont, Toray, Clothing Plus, Cityzen Sciences, Textronics, Interactive Wear, Vulpes Electronics.

This is the invisible arena that supplies every other arena. If you sell into smart clothing, these are the actual technology stacks underneath the brand names.

- Clothing Plus (Finland) and Cityzen Sciences (France) supply sensor-integrated textiles to consumer and clinical brands.

- Textronics (Mumbai) has leveraged Indian textile manufacturing to become an IoT hub for accessible smart monitors, with projected 16.2% growth in APAC.

- Interactive Wear specializes in flexible conductive fabrics, connection components, and modular electronics platforms that brands license and rebrand.

- AiQ Smart Clothing (Taiwan) spins conductive stainless-steel fibers with cotton for wearability, supplying multiple consumer and industrial clients.

The EU’s Ecodesign for Sustainable Products Regulation (ESPR), effective July 18, 2024, introduced digital product passports for textiles and prohibits the destruction of unsold textiles for large enterprises by July 19, 2026. That regulation falls hardest on the platform layer, where material traceability gets compiled.

The buyer: Product engineering VPs, CTOs and materials R&D leads, and OEM procurement. Long consultative sales cycles, contract manufacturing relationships, and reference deployments win the business.

The Five-Arena Framework: Why This Matters for B2B Go-to-Market

Here’s the actionable takeaway: if a demand gen team builds a list of smart clothing decision-makers and sends a single, one-size-fits-all message, the response rate will be poor. Not because smart clothing buyers don’t exist, but because there are five distinct buyer universes, each with its own titles, trigger events, and buying criteria.

The Five-Arena Framework for smart clothing ICP design:

| Arena | Primary Buyer Titles | Trigger Events | Content That Converts |

|---|---|---|---|

| Consumer Fitness | CMO, DTC Director, Retail Category Manager | New product line launch, wearable partnership announcements | Performance benchmarks, CAC case studies |

| Clinical Biometrics | Chief Medical Officer, Digital Health VP, Clinical Research Director | FDA clearance, pilot study completion, reimbursement code expansion | Validation studies, regulatory white papers |

| Defense and Industrial | Defense Procurement Officer, Occupational Health Director, HSE Manager | Contract renewal cycles, workplace safety mandates | Compliance documentation, field trial results |

| Luxury and Fashion | Fashion Innovation Lead, Creative Director, PR Director | Fashion week, flagship store refresh, collab announcements | Brand partnership case studies, editorial coverage |

| Materials and Platform | VP Engineering, R&D Lead, OEM Procurement | Product roadmap gates, material certification renewals, ESPR compliance deadlines | Technical specifications, reference deployments |

Each of these buyer groups requires its own distinct list, messaging approach, and content strategy. This segmentation process is exactly the type of foundational work that needs to be done before a campaign goes live. TAM, SAM, and SOM analysis are crucial for fragmented markets like this. Targeting the right buyers with the right context is more important than simply reaching more people.

How Span Global Services Supports This Approach:

Span Global Services enhances this segmentation by providing verified contact databases across all five arenas, enriched with firmographic and technographic signals tied to real buying intent.

In markets like smart clothing, data verification and profiling are the keys to successful campaigns. Without accurate targeting, campaigns risk consuming budget without converting leads. The right data is not just an advantage; it’s a requirement to avoid wasted spend and drive real results.

FAQs

What are the top smart clothing companies in 2026?

Top smart clothing companies in 2026 include Nike, Adidas, and Under Armour in consumer fitness; Hexoskin and Epicore Biosystems in healthcare; and DuPont and Toray Industries in e-textiles and materials.

Which industries are adopting smart clothing technology the fastest in 2026?

Healthcare, defense and industrial safety, and consumer fitness are the fastest adopters of smart clothing technology in 2026. Healthcare leads in remote monitoring, defense focuses on safety and performance, and consumer fitness drives wearable fashion adoption through performance tracking and connected apparel.

What is the difference between smart clothing and wearables like smartwatches?

Wearables are discrete devices worn on the body (watches, rings, headbands). Smart clothing integrates sensors and electronics directly into the garment itself using conductive fibers, embedded circuits, or textile-integrated sensors. The industry trend in 2026 is toward garments that perform machine learning inference internally, eliminating the need for a separate device.

Is smart clothing actually profitable for brands, or is it a marketing play?

Profitability depends on the arena. Clinical biometrics (Hexoskin, Epicore) and materials platforms (DuPont, Toray) operate on strong industrial margins. Consumer fitness smart clothing struggles with unit economics at scale due to return rates, battery life complaints, and washability concerns. Luxury and fashion crossovers are typically PR plays subsidized by brand marketing budgets.

How accurate is smart clothing compared to medical-grade equipment?

Validation depends on the product. Peer-reviewed studies have found Hexoskin biometric shirts comparable to medical pneumotachograph and Polar H7 heart rate sensors. Sensoria’s textile pressure sensors have been validated as a low-cost alternative to stabilometric platforms in posturographic assessment of patients with Parkinson’s disease. Accuracy varies significantly across brands, and medical applications require FDA clearance or equivalent regulatory approval.

What regulations are shaping the smart clothing market in 2026?

The EU Ecodesign for Sustainable Products Regulation (ESPR), effective July 18, 2024, introduced digital product passports for textiles. Large enterprises will be prohibited from destroying unsold textiles beginning July 19, 2026. In the U.S., FDA oversight applies to any smart clothing making medical claims. Defense procurement has its own certification pathways through DoD field trial programs currently underway.

Related Posts