Wearable IoT has quietly become one of the most consequential technology categories of the decade. What started as consumer fitness trackers has matured into a $185 billion global market spanning healthcare, manufacturing, logistics, defense, and enterprise workforce management.

For B2B marketers, this shift matters for one specific reason: the buyer universe for wearable-adjacent products has fundamentally changed, and most go-to-market teams have not caught up.

If your product integrates with wearables, sells into companies deploying them, or competes in the broader connected device ecosystem, this article covers what you need to know in 2026.

What Counts as a Wearable IoT Device in 2026

The category is broader than most marketers assume.

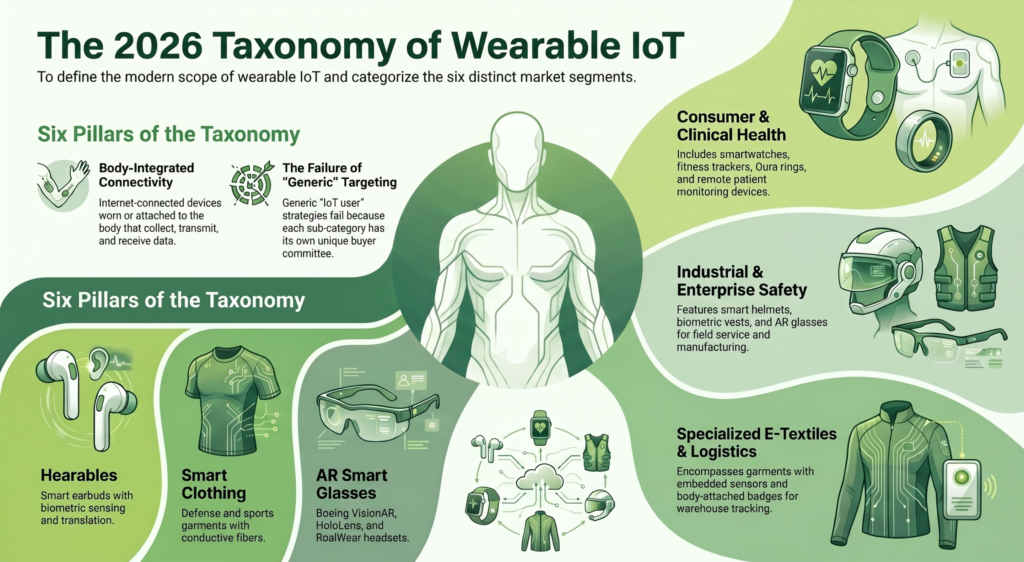

A wearable IoT device is any internet-connected device designed to be worn on or attached to the human body, capable of collecting data, transmitting signals, and often receiving commands from external systems.

That definition now encompasses seven distinct sub-categories:

- Smartwatches and fitness trackers. Apple Watch, Garmin, Fitbit, Samsung Galaxy Watch. The consumer-facing layer most people associate with wearables.

- Health monitoring wearables. Oura Ring, Whoop, continuous glucose monitors, cardiac patches, remote patient monitoring devices. Used extensively in clinical and workplace wellness contexts.

- Industrial safety wearables. Smart helmets, biometric vests, exoskeletons, fatigue monitoring bands deployed in oil and gas, mining, construction, and heavy manufacturing.

- Augmented reality smart glasses. Boeing VisionAR, Microsoft HoloLens, Magic Leap, RealWear. Used for manufacturing, field service, and training.

- Smart clothing and e-textiles. Garments with embedded sensors, conductive fibers, and textile-integrated electronics. Emerging fast in defense, sports, and clinical monitoring.

- Hearables. Smart earbuds with biometric sensing, translation, and workplace communication features.

- Body-attached asset trackers. Worn badges and wristbands used in warehouse, hospital, and event logistics to track worker location and activity.

Each sub-category has its own buyer committee, procurement cycle, and technology stack. This complexity is precisely why generic “IoT users” targeting fails in this space and why precision targeting compounds so effectively.

The Market Numbers That Matter

Wearable technology market sizing varies across analyst firms because the category definitions differ, but the directional numbers tell a consistent story.

‘MarketsandMarkets’ pegs the global wearable technology market at $84.53 billion in 2025, growing to $176.77 billion by 2030 at a 15.9% compound annual growth rate.

Precedence Research puts the broader e-textiles and smart clothing segment at $22.08 billion in 2025, forecast to hit $274.99 billion by 2034 at a 32.34% CAGR.

‘Grand View Research’ tracks smart clothing specifically at $7.40 billion in 2026, growing at 26.8% CAGR through 2033.

What these numbers obscure is where the real buying power sits. Consumer wearables generate headline revenue, but B2B deployments generate the enterprise contract values that matter for B2B marketers.

A single smart helmet rollout across an industrial workforce of 10,000 employees represents a larger contract than thousands of consumer smartwatch purchases combined. The enterprise segment is where targeting precision pays off most dramatically.

The Five Industries Driving B2B Wearable Adoption

Generic industry segmentation will lead you astray in this market. Adoption patterns cluster around five specific verticals, each with distinct use cases, decision-makers, and buying windows.

Healthcare and clinical monitoring. Hospitals, health systems, and remote patient monitoring providers deploy wearables for continuous vitals tracking, chronic disease management, post-surgical recovery, and clinical trials. The buyer committee includes Chief Medical Officers, CIOs, and HIPAA compliance leads. Deployment cycles are long, but contract values and renewal rates are exceptional.

Manufacturing and industrial operations. Boeing, Siemens, Caterpillar, and hundreds of manufacturing enterprises deploy AR smart glasses, biometric vests, and fatigue monitors to improve safety, productivity, and quality control. Buyer committee: VP Manufacturing, Head of Operations, HSE Director, Digital Transformation Lead. Enterprise case studies show documented ROI in injury reduction, training time, and error rates.

Oil, gas, and mining safety. BP, Shell, Rio Tinto, and major extraction operators deploy environmental and biometric wearables to protect workers in hazardous conditions. The business case is straightforward: workplace injury costs exceed $60 billion annually in the US alone. Wearables that prevent even a fraction of incidents pay for themselves within quarters, not years.

Retail and warehouse operations. Amazon, Walmart, DHL, and logistics operators use wearables for inventory tracking, workforce productivity, and employee wellness programs. Use cases range from scanner gloves to biometric monitoring for heat stress in fulfillment centers.

Defense and public safety. Military, first responders, and security operations deploy ruggedized wearables for tactical communication, physiological monitoring, and situational awareness. This vertical has the most demanding procurement standards and highest per-unit contract values.

For B2B vendors selling into any adjacent technology category (IoT platforms, analytics, cybersecurity, workforce management, cloud infrastructure), these five industries represent the highest-value account lists to build.

Why B2B Marketers Keep Missing This Audience

Three common failure modes destroy targeting ROI in the wearable IoT space.

Failure 1: Treating wearables as a monolithic category. A CMO at Nike, a Chief Medical Officer at a hospital system, and an HSE Director at an oil major are all wearable buyers in the broadest sense, but they have nothing in common operationally.

Lists built on broad wearable technology adopter flags produce campaigns where the messaging fits nobody. Precision requires segmenting by use case and vertical, not just by technology presence.

Failure 2: Targeting the wrong decision-maker. Most generic tech lists default to CTO and VP Engineering contacts.

In wearable IoT, procurement authority is distributed across Operations leaders (industrial and manufacturing use cases), Medical and Clinical leaders (healthcare), HR and Benefits leaders (corporate wellness), and Safety and Risk leaders (hazardous industries).

Vendors still pitching exclusively to IT decision-makers are talking to the wrong people in 60 to 70 percent of enterprise deployments.

Failure 3: Ignoring deployment maturity signals. A company running a 100-person pilot has a completely different buying posture from one scaling a 10,000-employee rollout. The first is looking for technical fit and proof-of-concept flexibility. The second is looking for enterprise-grade integration, compliance certifications, and multi-year support contracts.

Generic lists do not distinguish between these, so outbound messaging misses in both directions.

The solution in every case is the same: segment by use case and deployment stage, not by firmographic proxies.

How to Build a Precision Targeting Engine for Wearable IoT

A targeting engine that actually converts in this market has four layers.

The first layer is industry vertical segmentation that maps directly to use cases. Healthcare clinical monitoring, industrial safety, warehouse operations, corporate wellness, and defense. Each vertical gets its own ICP definition, messaging track, and campaign calendar.

The second layer is decision-maker intelligence anchored to the actual buying committee for wearable adoption. CIOs matter, but so do Medical Directors, HSE Leads, VP Operations, and Benefits Administrators. The weight of each role shifts by use case, and your targeting data needs to reflect that.

The third layer is deployment signal enrichment. Job postings mentioning specific wearable platforms, press releases announcing pilots, case studies confirming scale, and public procurement filings all reveal deployment maturity. Enriching your target account list with these signals separates pilot-stage buyers from production-stage buyers and routes outbound messaging accordingly.

The fourth layer is stack co-adoption mapping. Companies deploying industrial wearables are also buying IoT platforms, analytics software, cybersecurity solutions, and MES integrations. If your product sits adjacent to wearable deployments, knowing which complementary technologies an account already runs transforms “cold prospect” into “warm integration conversation.”

The companies winning revenue in this market are not the ones with the biggest outbound teams. They are the ones whose targeting infrastructure combines these four layers into actionable segments that their SDRs can actually execute against.

The Content and Campaign Plays That Work

B2B marketing in the wearable IoT space has three campaign patterns that consistently outperform.

Vertical-specific case study marketing. Generic wearable ROI content gets ignored. Content that leads with named enterprise deployments (“How Boeing Cut Wiring Task Times by 25% with AR Wearables”) gets read, shared, and cited by AI search engines.

If you are targeting manufacturing buyers, your content engine should be producing manufacturing-specific wearable case studies, not cross-industry thought pieces.

Use-case-driven webinars and executive briefings. CFOs in oil and gas do not attend wearable technology innovation webinars. They attend “How Biometric Monitoring Reduced Hazard Insurance Costs by 18% at Major Operators” briefings. The specificity of the use case drives attendance and conversion.

ABM campaigns built on verified technographic signals. The highest-performing campaigns in this space are account-based programs that start with a verified list of companies confirmed to be deploying specific wearable platforms.

A vendor selling cloud infrastructure to manufacturing AR users runs a different play than a vendor selling compliance software to clinical wearable operators. Pre-segmenting the account list by platform, use case, and deployment stage is what makes ABM work in this market.

All three patterns depend on one thing: verified, up-to-date data on who is actually deploying wearables and at what stage. That is the input that turns a generic B2B marketing engine into a specialized wearable IoT targeting machine.

Where Span Global Services Fits In

Span Global Services maintains 100% verified Wearable Technology Users Lists covering companies across all five major B2B wearable adoption verticals.

The database includes decision-makers’ contact intelligence across IT, operations, clinical, safety, and wellness functions, with segmentation by use case, vertical, company size, and geography.

For B2B marketers looking to sharpen their wearable IoT targeting, we have published a series of deep dives across the category.

- Our analysis of top companies using wearable technology walks through real enterprise deployments at Boeing, BP, and others, with specific implications for B2B outreach.

- The smart clothing technology in 2026 guide breaks down the five market arenas and identifies where the highest-value buyers sit.

- And our consumer-side comparison of the Oura Ring versus Apple Watch for health tracking unpacks how the health monitoring wearable category is evolving, with implications for HR, benefits, and corporate wellness teams.

Used together, these resources map the full commercial landscape of wearable IoT: the platforms being adopted, the companies deploying them, and the buyer personas driving procurement.

Frequently Asked Questions

What is the difference between wearable devices and wearable IoT?

A wearable device is any electronic device designed to be worn on the body. Wearable IoT specifically refers to wearables that are internet-connected, capable of transmitting data to cloud systems, and often integrated with broader enterprise or consumer platforms. Most modern wearables qualify as IoT devices, but the distinction matters when B2B buyers are evaluating platforms for data aggregation, integration, and analytics.

Which industries are the biggest B2B buyers of wearable IoT in 2026?

Five verticals dominate B2B wearable IoT adoption: healthcare and clinical monitoring, manufacturing and industrial operations, oil and gas safety, retail and warehouse logistics, and defense and public safety. Each vertical has distinct use cases, decision-makers, and deployment models, which is why precision segmentation by vertical matters more than generic firmographic targeting.

Who are the decision-makers for wearable IoT purchases at enterprise accounts?

Decision authority varies by use case. Industrial and manufacturing deployments typically involve VP Operations, HSE Directors, and Digital Transformation Leads. Healthcare deployments involve Chief Medical Officers, CIOs, and compliance leaders. Corporate wellness programs run through HR and Benefits leaders. Defense and public safety involve procurement officers and specialized technology evaluators. CIOs are often part of the committee, but rarely the sole decision-maker.

How do B2B marketers verify which companies are actually deploying wearable IoT?

Verification relies on multiple signals: public case studies and press releases, job postings mentioning specific wearable platforms, procurement filings, technographic web fingerprinting, and direct vendor customer references. Quality B2B data providers cross-reference multiple sources to distinguish genuine deployments from marketing announcements or pilot-stage experiments.

What campaign strategies generate the best ROI when targeting wearable IoT users?

Three campaign patterns consistently outperform in this market: vertical-specific case study marketing that cites named enterprise deployments, use-case-driven executive briefings rather than generic innovation webinars, and account-based marketing programs built on verified technographic signals. All three require precision targeting data as an input, which is why generic “IoT adopter” lists rarely produce a strong pipeline in the wearable category.

The Takeaway

Wearable IoT has evolved from a consumer novelty into a serious enterprise technology category with well-defined verticals, buyer personas, and deployment patterns.

B2B marketers who continue to treat the market as a one-size-fits-all segment will continue to lose pipeline to competitors who have mastered segmentation by use case, decision-maker, and deployment stage. The market rewards precision, and precision starts with the data infrastructure behind your targeting engine.

The opportunity in 2026 is not whether wearable IoT will matter for B2B. It already does. The opportunity is whether your go-to-market team is set up to target it with the specificity ands resources the category demands.

Related Posts